Swank v0.05.00

Supply and Demand

a.k.a. microeconomics

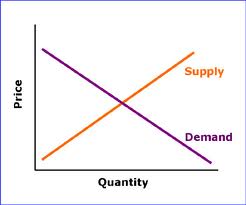

Demand: the more available, the lower the price. air is abundant and free. diamonds are scarce and expensive. (function of quantity?) Or, the higher the price, the fewer will be sold (function of price).

Supply: (hard to justify as a function of quantity try) as the price goes up, more quantity will be made available. Oil is a good example. (function of price?)

Consider other slopes. Vertical supply curve (only X number in existance). Horizonal supply curve (price fixed by government or cartel). Irish potato (during the famine) is said to have a upward sloping demand curve: as the price increased, buyers could afford less meat, and needed more of the staple. Downward supply curve: the prototype cost $1M, but each mass-produced item costs $100 (economists say the slope will go back up if the quantity is high enough).

No units on axis. All we describe are the general slope. Real supply curves are uneven (e.g. oil again).

Shifts in the curves or changes in supply or demand.

[ask class to think of factors which affect the supply and demand curve]

Increased demand from a factor other than price is a shift in the entire curve. Example factors are advertising, changing tastes and fashions, incomes (changes in disposable income), price changes in complementary and substitute goods, market expectations, and number of buyers.

Similarly for supply. The usual example is technology changes (increasing supply). Natural disasters (decreased supply).

The four basic laws of supply and demand are:

- If demand increases and supply remains unchanged, then it leads to higher equilibrium price and quantity. (D up, P up)

- If demand decreases and supply remains unchanged, then it leads to lower equilibrium price and quantity. (D down, P down)

- If supply increases and demand remains unchanged, then it leads to lower equilibrium price and higher quantity. (S up, P down)

- If supply decreases and demand remains unchanged, then it leads to higher price and lower quantity. (S down, P up)

Interventions

Price Ceiling. Above equilibrium has no effect. Below makes demand higher than supply, and a scarcity results.

Minimum wage. Worker is the supplier of labor. Business the consumer/demander. Supply is higher than demand, resulting in a glut of labor, i.e. unemployment.